Discover the benefits and potential of quant investing, a strategy that uses mathematical models and advanced algorithms to make investment decisions. Learn how it is outperforming traditional strategies and shaping the future of finance.

Over the past couple of months, investors’ interest in quant investing or algo investing has significantly increased. It is a methodical, rule-based approach to stock selection. The entry and exit points and the amount of each investment should all be explicitly specified in the criteria.

As an illustration, you ranked every stock according to its performance over the previous 12 months. The top 10 stocks with the best returns are chosen, and they are then given equal weights.

Contents

Here are the steps involved in Quant Investing:

Step 1:

The selection of the universe of stocks is the initial stage in creating quant-based models. If you only want to concentrate on large-size companies, you could use the Nifty 50, or if you’re going to build multi-cap portfolios, you could use the BSE 500.

Step 2:

Back-testing the investing hypothesis is the next stage. One theory is that equities with momentum typically maintain that momentum. You arrange stocks based on their momentum during the last several weeks or months, then choose the stocks with the highest momentum.

You arrange stocks based on their momentum during the last several weeks or months, then choose the stocks with the highest momentum.

Step 3:

The third step is to give weights to these stocks. Giving them identical weights is one of the simplest methods to do this. For example, if you have chosen ten stocks, you would give each stock 10% weight. You could also strive to maximize the risk-adjusted returns for these ten stocks or assign them weights based on their momentum scores.

Systematic investing is an investment strategy that builds portfolios using a set of rules. It employs automated data-driven insights and sophisticated computer modeling approaches that provide several benefits over the conventional approach.

The driving force behind your strategy’s performance is the criteria you use to choose which stocks to buy.

Macroeconomic factors like GDP growth, interest rates, inflation, or the value of a currency in relation to the USD might be included in this list. Popular style factors include value, momentum, quality, low volatility, and others.

Cons of conventional investing

It is important to understand the problem areas of traditional investments to appreciate the beauty of quant investing.

If we look at traditional investments, we see that a fund manager and team members conduct an in-depth analysis of businesses and industries before creating a portfolio. It entails examining both qualitative and quantitative aspects, such as a company’s financial statistics and pricing, as well as managerial competency and a sector’s competitiveness. But ultimately, whether or not to invest in a firm depends much more on personal preferences. This strategy has several clear disadvantages, despite its inherent benefits.

Here are a few such disadvantages.

The physical reality of fund managers: The physical reality of a human being is one issue with discretionary investment. In such an investing strategy, your fund manager is responsible for a lot of things, from finding investment opportunities to building your portfolio to generating profits.

But everyone is aware that computers can do far better than humans if the elements on which we are based our judgments can be quantified.

Subject to Human Prejudice:

When people are involved, it’s common for personal opinions and biases to come into play. The field of investments is no different than other areas where our biases invariably pop up.

If we look from an investment angle, a company or an investment that is beneficial to you may be overlooked by your fund manager due to personal prejudice. Here, every little decision counts. So, poor judgment by your fund manager might lead to lower-than-expected returns.

Fund management expertise determines returns:

A problem with discretionary investing is that it relies on the skills and knowledge of the people managing the investments, especially the fund manager. It is because he will ultimately make the investment decisions. If the fund manager does not have the necessary information, abilities, and market experience, your portfolio might take severe damage.

How can Factor Investing address these issues?

In the case of Factor Investing, you are independent of a single fund manager’s abilities, expertise, and experience. Instead, a group of qualified managers researches to optimize your portfolio. Your portfolio will likely be built better, generating greater returns, as more fund managers collaborate to develop portfolios and contribute their talents and knowledge.

Scientific method: The systematic investment technique is very different from traditional investing methods. According to factor investing, market prices move in observable and predictable patterns rather than randomly. Systematic investing uses high-quality big data, data science, data mining, and scientific testing of investment concepts to make an investment choice.

For instance, historical price data may be examined while excluding certain markets and periods before you make any investing decisions. The test can then be repeated using the markets and times that were previously omitted. This approach aids in lowering the risks associated with an investment choice.

Wise investment decisions: Systematic investing goes above and beyond the discretionary investing approach’s commitment to recommending fundamentally solid investment choices. It selects the best investment ideas and eliminates the others using sophisticated modeling approaches. This method enhances human judgments rather than ignoring them. In addition, it eliminates emotions that influence the possibility of your investment portfolio.

Scalability: By creating well-diversified portfolios with various assets, systematic investing protects you from concentration risk. Better investment strategy implementation is possible with automated, speedy processing of fresh data while controlling risk factors.

Superior targeted outcome: Investors may have considerably better control over the performance of their portfolios with the aid of systematic investing. For instance, a trader trying to lower volatility in his portfolio may think about buying stocks with low volatility. Using these rule-based techniques, investors may improve their portfolios for a better risk-return trade-off.

The pioneer of quant investing in India, Estee Advisors, has created Gulaq portfolios based on quant investing. Let’s explore how Estee’s quant investing is outperforming traditional investing strategies.

Benefits of Estee’s Multi-factor Approach

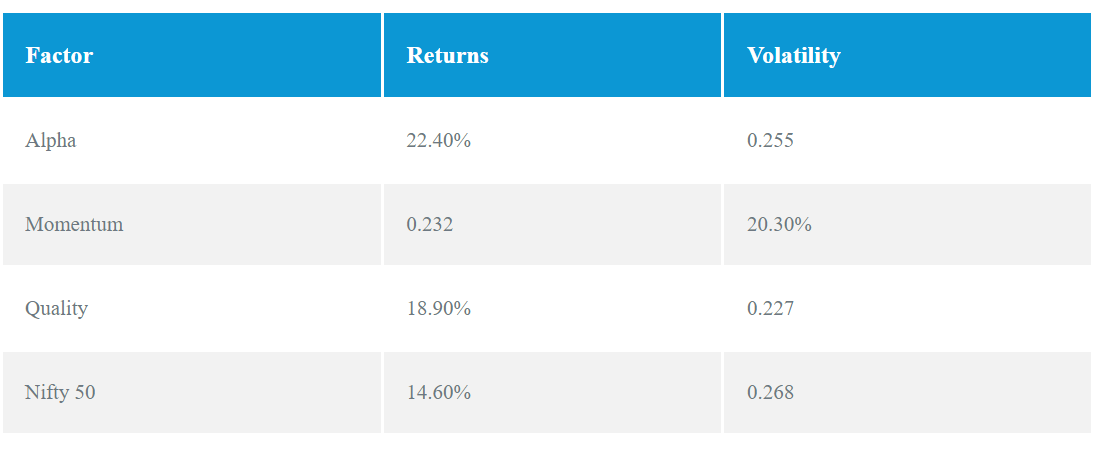

We can infer from a quick glance at previous factor-based indexes that they have consistently outperformed the index while also exhibiting lower volatility.

Long-term risk adjusted returns are improved by diversifying across these factors. Let’s examine this carefully. Momentum, one of the elements with the best performance across all locales, generally performs well when the markets are moving but will continue to produce noisy signals when they are range-bound.

During bear markets, variables like quality and low volatility often perform well, but during bull markets, elements like size and expansion typically do well.

Like how an index is formed, we harness the cyclicity of elements across various market circumstances to generate a diversified portfolio. Like in an index, if a stock is underperforming, it is removed and replaced by one that is performing better. The elements that are not appropriate are omitted, while those that are functioning well and are expected to continue performing well under the present market conditions are included.

This enables us to produce consistent returns across market cycles.

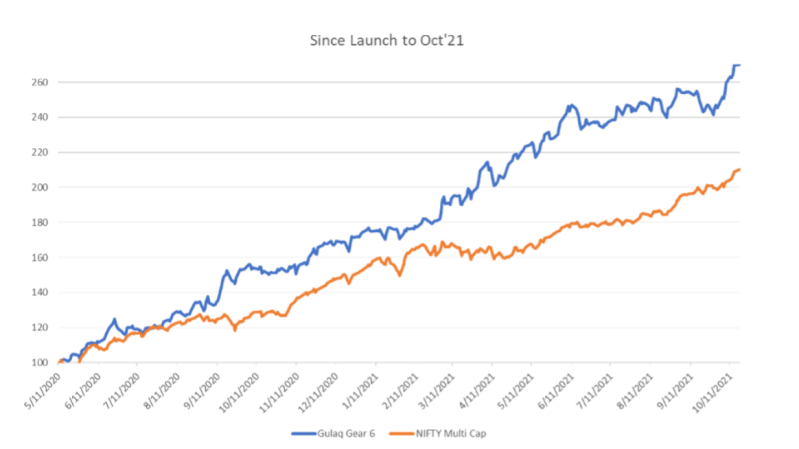

As we can see in the chart below, markets have been falling since October 2021 and are currently down around 5% from their top, but because to the successful switch to efficient factors, our portfolios have been able to provide positive returns of 12%.

From our inception in May 2020 through October 21, we consistently create alpha, even in bull markets.

Final Thoughts

Many of these rule-based investment techniques, such as factor-based ETFs and curated stock baskets, have found favour with investors. Awareness of these systematic strategies and their advantages in all market circumstances has greatly improved.

This is encouraging for the financial services sector’s future. Investors have to commit a portion of their capital to quant-based investment strategies in order to benefit from the scientific rule-based approach and diversify beyond traditional investments.